Check Your Credit Before Buying a House

Published: February 26, 2015 | 5 min read

Buying a home is one of the most stressful events, but you can ensure a smoother process by making sure your credit is in good shape before applying. Here are three reasons why you should check your credit before buying a house.

1. Your score isn’t as high as you think

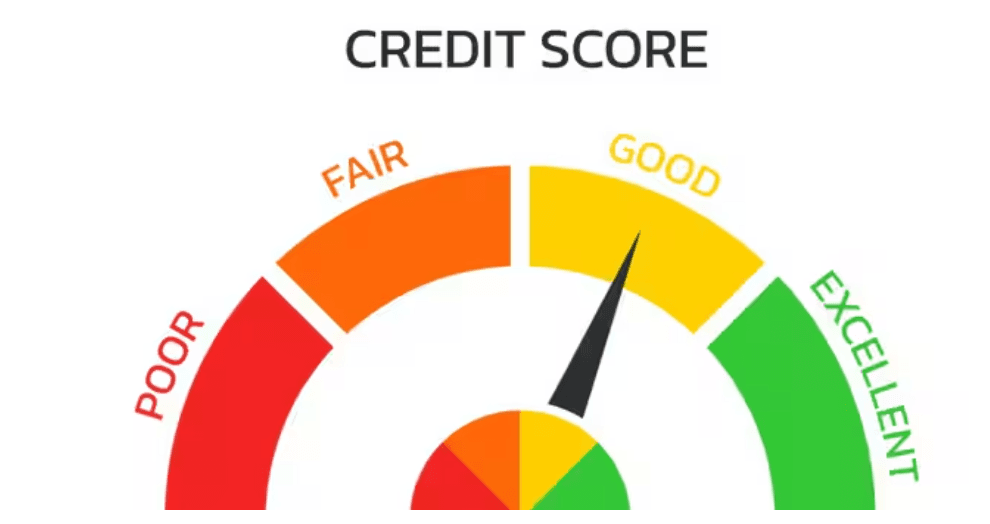

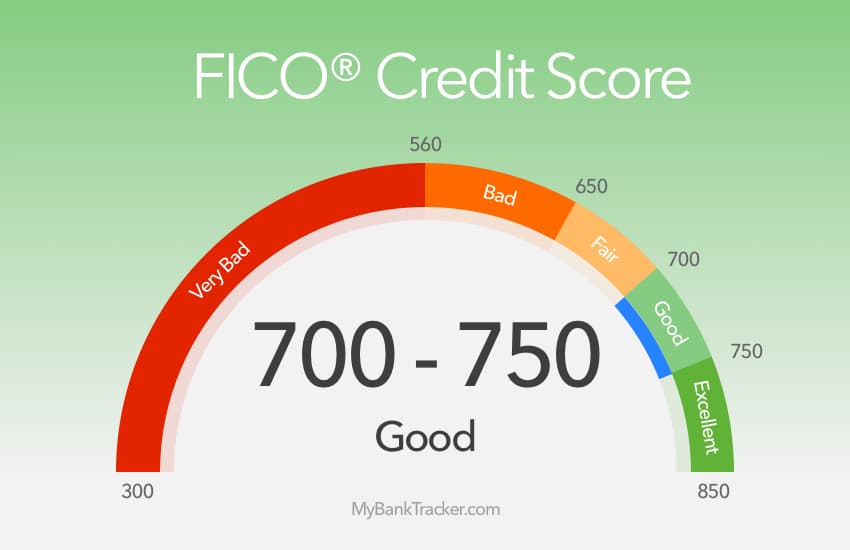

Even if you know the importance of good credit, there's a chance your credit score isn't as high as you think. About eight years ago, it was possible to get a conventional mortgage loan with a credit score as low as 500.

Today, many conventional lenders require a minimum score of at least 680. Paying your bills on time every month does not guarantee a high credit score. Other factors can bring down your score, such as too much credit card debt, too many credit inquiries and a short credit history.

Check your credit report and score (annualcreditreport.com) before applying for a mortgage, and then take steps to raise your score. It’ll be easier to qualify for a mortgage and you'll qualify for the most favorable interest rates.

2. Identity theft is one of the fastest growing crimes

If you never check your credit, you could be a victim of identity theft without even realizing it. This is one of the fastest growing crimes affecting millions of people each year.

If someone gets hold of your personal information, they can open credit accounts in your name and completely destroy your credit history. And unfortunately, you can’t qualify for a mortgage until you fix the situation.

Depending on the damage, it can take years to resolve identity theft and clean up your credit. If you check your credit regularly – at least once a year – you can detect signs of identity theft before it ruins your credit reputation.

3. Creditors aren't perfect

Creditors report your account activity to the credit bureaus every month, but this doesn’t mean the information is always accurate. Creditors can make mistakes, such as updating your report with erroneous information, which can bring down your credit score and make it harder to buy a house.

Check your credit report for errors, and immediately notify you creditor of any mistakes. By law, your creditors have to investigate any complaints. If your creditor isn't cooperative, dispute errors with the credit bureaus or file a complaint with the Federal Trade Commission.

Your credit report provides details about your credit history, and many lenders will use the information in your report to determine whether you're eligible for a loan. You’ll need to closely monitor your credit activity and make sure your report contains accurate information.

Get Pre-Qualified in 60 Seconds!

Find out what you can afford with no hard credit check, just a few simple questions.

Select the type of loan that best fits you