Turn That Mortgage Rejection into an Acceptance

Published: November 12, 2015 | 5 min read

You’re probably eager to jump into homeownership. Unfortunately, plenty of things can derail a home purchase, and they happen with surprising regularity. In 2013, about 14.5% of all new purchase loans were denied by lenders, and that number climbed to 22.7% for refinances.

Reasons your application may be rejected

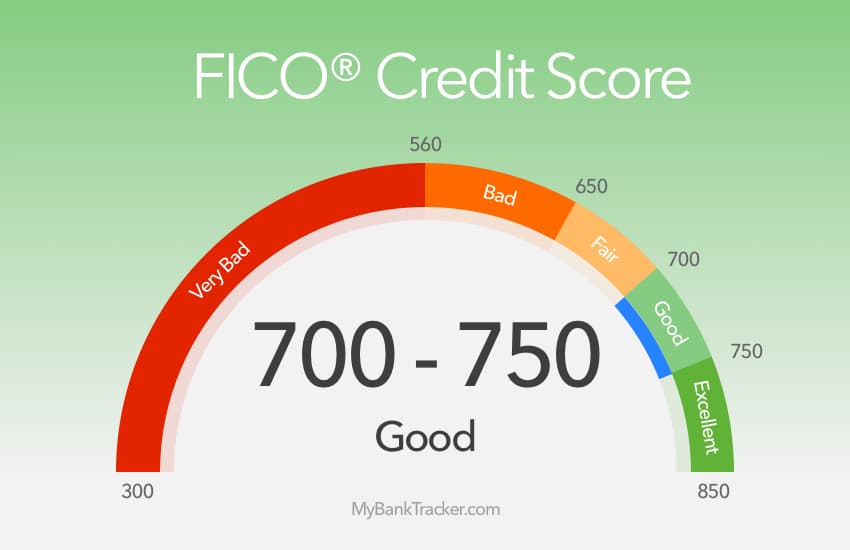

A mortgage rejection can be frustrating and discouraging, but it doesn’t mean you’ll never be able to buy your own place. Here’s a look at six of the biggest threats to homeownership. Co-signing loans Whether it’s your child, your sibling, or your best friend, cosigning a car loan, a student loan or any other loan for another person can threaten homeownership. This is because that loan shows up on your credit report and you’re listed as a joint borrower. Even if you’re not the primary account holder, you will be held responsible for the loan if the primary borrower defaults. This increases your debt-to-income ratio. Unfortunately, the more debt you have in your name, the less you’re able to borrow when buying a home. In some cases, cosigning a loan can push your debt-to-income ratio over the limit allowed by a lender, which can keep you from getting a mortgage, period, until the debt is no longer in your name. Job-hopping You might be a free spirit who loves to change jobs every six months to 12 months. But unfortunately, from a lender’s viewpoint, you’re not stable enough to buy a home. Lenders want to see steady income and employment. Ideally, you should stick with the same employer for at least 24 months before applying for a mortgage. If you must switch jobs, remain in the same field and make sure your new salary increases or stays the same. Not having a large enough savings account Nowadays, lenders don’t only ask to see paycheck stubs and tax returns. They also request bank account statements. They’ll look at your savings accounts and other assets to see whether you have enough funds for a down payment and closing costs. And if you don’t have a sizable savings account, a lender might reject your application until you’re able to build your fund. Not enough credit activity If you get a credit card to build your credit history, make sure the bank issuing your card reports to the credit bureaus on a regular basis. When applying for a mortgage, the bank will check your credit history, and non-existent credit can be just as problematic as bad credit. Before applying for a credit card or any line of credit, speak with creditors and make sure they’ll report your credit activity to the bureaus every single month. Credit report mistakes The worst thing you can do is fully trust your creditors to report accurate information on your credit report. Creditors make mistakes, and sometimes they report a late payment or a collection account in error. So you need to check your own credit report at least once a year for accuracy. If you notice an error, contact your creditor immediately to resolve the issue, or file a complaint with the credit bureaus. Credit report errors can reduce your credit score, potentially to the point where it’s too low to qualify you for a mortgage. Poor credit habits You can get a conventional mortgage with a credit score as low as 620 and an FHA mortgage with a credit score as low as 500, but your recent credit activity must be positive. For that matter, some banks will reject your mortgage application if you have more than one or two late payments in the past 12 months.Your next steps after rejection

But what do you do when you’ve already made a mistake, and you’re left with no mortgage and an impatient seller? Though your exact course of action will depend on your individual circumstance, there are ways to turn your rejection into an acceptance. Try a different tactic Occasionally, it is possible to turn around and apply with a different lender who has fewer restrictions. This is because some lenders tack additional guidelines onto those that are required by law, making it more difficult to qualify. On your second go around, try a local bank—they are often more willing to work with individuals. If that isn’t an option, you may want to consider applying for a different loan program. A normal 30 year fixed may be considered the standard, but that doesn’t mean it’s for you. Mortgages backed by the government—FHA, VA, and USDA loans—tend to have less strict requirements (FHA, for instance, allows a credit score as low as 580). Work on your credit Credit issues are one of the top reasons lenders reject loan applications. Often, people only realize their credit is a problem when the time comes to make a large purchase, but ideally, you would be keeping an eye on your credit situation well in advance. If your problem is your credit, start by paying off as many cards as you can (but don’t close them immediately—your score takes into account how much credit you have open to you vs. how much you’ve used). Even once you’ve cleaned up your act, it can take time for your credit to recover—one to three months, or even longer if you’ve done severe damage. Troubleshoot your appraisal Another very common reason loans are rejected is that the appraisal came in too low, leading the bank or lender to think that the property isn’t worth the investment on their part. Sometimes a low appraisal is a fluke. Often, all you can do is move on to a different lender, or, if it happens a second time, a different house. Find a cosigner If you’re having trouble qualify for credit, debt, or income reasons, asking a close relative to cosign the mortgage with you may be the helping hand you need. This isn’t always recommended, though, for reasons we’ve already talked about. Cosigners are legally responsible for the debt, too, which can raise their debt-to-income ratio and make it difficult for them to make large purchases in the future. Plus, money and family don’t typically mix well. The Bottom Line? There are plenty of potential setbacks on the road to buying a home. If you can identify potential threats to homeownership, it’ll be easier to make decisions that will help you reach your goal—and even then, all is not lost.Get Pre-Qualified in 60 Seconds!

Find out what you can afford with no hard credit check, just a few simple questions.

Select the type of loan that best fits you