home. it's finally here

buy with as little as 3% down*

supercharge your mortgage

technology engineered for a better mortgage process

Total Mortgage is changing lending for the better. Better technology means a quicker loan process. Awesome people make it painless.

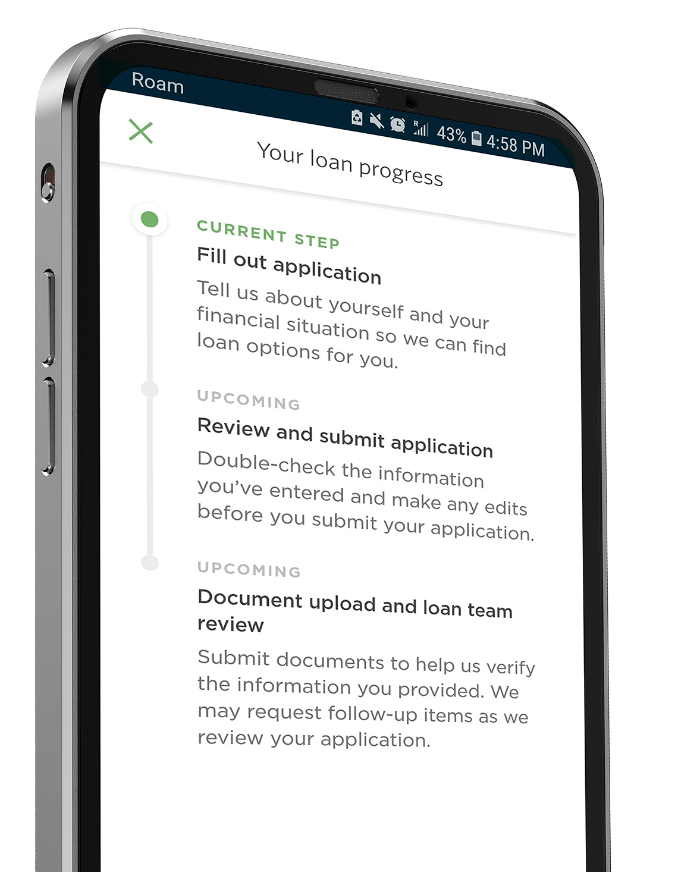

OUR TECHNOLOGY

crunch the numbers

Calculate payments, estimate your budget, and determine refinance savings in seconds.

Focus on the move, not the mortgage.

Greenlight your loan, and close in 21 days.*

Learn more

Kody D. .

"Lender was super informative and was able to get me the best rate in the shortest amount of time. I was a first time home buyer and we were able to close in 21 days! I have a wonderful experience and highly recommend Mark Lloyds services!!!"

find a pro in your state

We might be right in your backyard

Mortgage rates are volatile and subject to change without notice. All rates shown are for 30-day rate locks with two and a half points for a single family owner-occupied primary residence unless otherwise noted. The APR for adjustable rate mortgages (ARMs) is calculated using a loan amount of $417,000, two and a half points, a $495 application fee, $450 appraisal fee, $1,195 underwriting fee, $10 flood certification fee and a $82 credit report fee. Some rates and fees may vary by state.* Products are subject to availability on a state-by-state basis. All interest rates listed are for qualified applicants with 750 or higher FICO and 80 LTV over a 30-year loan term except where otherwise noted and are subject to mortgage approval with full documentation of income. By refinancing your existing loan, your total finance charge may be higher over the life of the loan.

*Terms and Conditions Apply. For complete details click here.