Understanding Mortgage Rates: How the Federal Funds Rate Affects Mortgage Rates

Published: December 5, 2016 | 5 min read

Eight times every year, the Federal Reserve’s Federal Open Market Committee (FOMC) meets to discuss and possibly alter their position on monetary policy.

There are several different courses of action they could take, the most common being quantitative easing, buying and selling government securities, and raising or lowering the federal funds rate.

Most recently, the fed’s tool of choice has been adjusting the federal funds rate.

Click here for today's mortgage rates.

What is the federal funds rate?

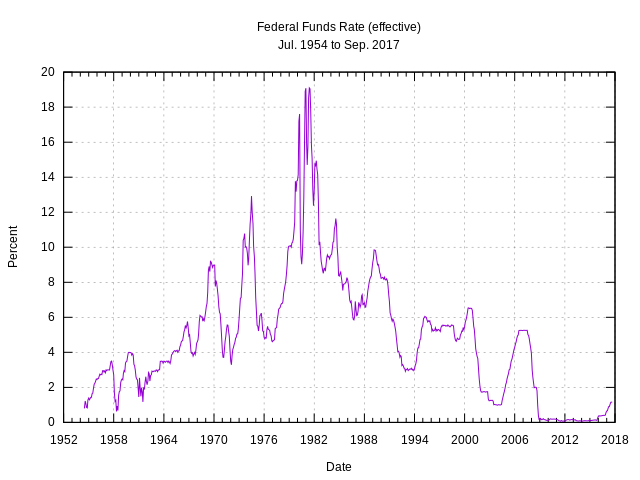

The federal funds rate is the rate at which depository institutions (banks and credit unions) charge each other for overnight deposits. Why would they need to lend each other money? All banks are required to have a certain amount of funds in their reserves (usually 10%), and sometimes customers withdraw enough money from the bank that the bank’s reserves are below the requirement. They now have two options: to borrow money from the fed or from another bank. The federal funds rate determines how much interest a bank will have to pay for that loan.

How the federal funds rate affects the economy

The federal funds rate is an important base rate that has trickle down effects on the entire economy. After all, if the federal funds rate goes up and banks have to pay more for overnight loans, then it goes to reason that they are going to have to make up the higher cost by raising their own rates. Conversely, if the federal funds rate is lowered, banks can pass lower interest rates on to their borrowers. With the benchmark federal funds rate lowered, rates on credit cards and business loans also decline, encouraging lending for both businesses and consumers. Businesses are able invest in infrastructure and hire more employees, while consumers make more payments on credit knowing that they don't get charged as much on the interest. This results in more financial transactions, ultimately contributing to economic growth of the nation at large. That's why when the Fed wants to promote economic growth they lower the federal funds rate, and when they think the economy can handle it, they raise the federal funds rate.Mortgage rates and the Federal Reserve

Understanding mortgage rates can be tricky. The way the situation with the Fed raising and lowering rates is portrayed in the news leads many people to believe that the Fed controls mortgage rates. This is not true—the Fed does not directly set mortgage rates at all. However, that’s not to say that it has no influence over mortgage rates.Fedspeak

At the Federal Reserve, the forward guidance “fedspeak” that officials offer up to the markets is one of the most powerful tools they have. It’s actually a little bit of the opposite of that old saying that “Actions speak louder than words.” Generally, when a fed official comes out and gives even the slightest hint that they are in favor of rising rates, investors move away from “safe” government bonds and into riskier assets like stocks. That’s good for the economy, but it causes mortgage rates to rise. As we’ve seen several times this year, the fed can create a buzz about raising the fed funds rate (which can drive up mortgage rates), but then retreat back from that position and not raise rates (causing rates to fall back down). It’s this cat and mouse game of talking and not delivering that has landed the Fed in hot water, with some critics claiming the Fed has a credibility problem. Regardless of whether or not you agree with them, it’s undeniable that what the Fed says can influence markets. Click here for today's mortgage rates.How mortgage rates are actually set

If the Federal Reserve doesn’t set mortgage rates, who does? Good question. Just as is the case with many other aspects of the economy, market forces are to thank (or blame). Most of the action takes place on the secondary market, where mortgage-backed-securities (MBS) are bought and sold. These mortgage bonds have prices and yields that move up and down just like stocks and bonds do. If the economy is performing well, investors expect higher yields, and vice versa when the economy is under-performing. So in a way, mortgage rates are a reflection of how well the economy is doing. Specifically, the three major drivers of mortgage rates are:- Stock prices

- The labor market

- Inflation

Bottom line

When you're trying to understand mortgage rates, remember: the Federal Reserve and the federal funds rate do not control mortgage rates. There are several other economic factors at play that anyone trying to track and predict where mortgage rates are going should pay attention to. That being said, the Federal Reserve does play a major role by influencing how the economy functions, and it's always important to keep an ear out for what they're saying.1. chart via wikipedia

Get Pre-Qualified in 60 Seconds!

Find out what you can afford with no hard credit check, just a few simple questions.

Select the type of loan that best fits you